The Personal Electronics Perfect Storm

Why 2026 is becoming a defining stress test for personal electronics

For years, personal electronics benefited from broad component availability, efficient global trade and relatively manageable pricing. In 2026, that model is under strain. Energy volatility, tariff uncertainty, AI-led component allocation and renewed inflation in memory and processors are now hitting the same market at the same time - tightening margins, weakening planning visibility and reducing room for error.

AT A GLANCE

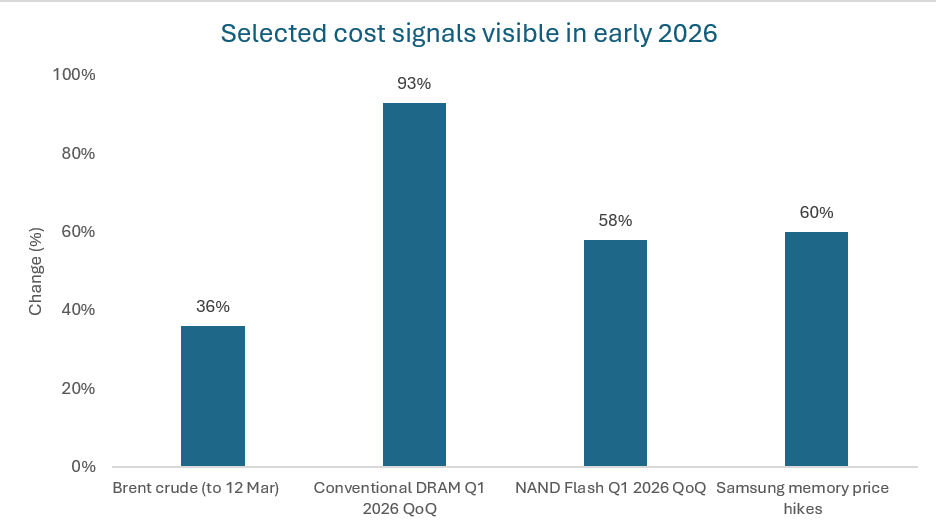

• Brent crude rose by more than 36% after the USA and Israel attacked Iran on February 28, briefly topping $119 intraday.

• Some forecasts point to DRAM and NAND contract-price increases of around 80%-90% in Q1 2026 compared to Q4 2025.

• Outman expects average PC prices to rise by 15% YoY in 2026, with more pessimistic scenarios closer to 20% for major brands.

• Samsung raised memory-chip prices by up to 60% compared to September as shortages worsened.

• Lead times for some server CPU orders have reportedly stretched by as much as six months.

WHY THIS MATTERS NOW

The disruption visible across electronics is no longer abstract. It is showing up in higher component costs, less predictable lead times, more volatile pricing and a procurement environment with far less room for error. When oil rises, freight, packaging, plastics and factory operating costs rise with it. When tariffs shift, sourcing decisions and landed costs can change overnight. When AI demand takes priority, consumer OEMs do not necessarily lose access to supply, but they do lose bargaining power.

A MARKET UNDER PRESSURE FROM FOUR DIRECTIONS

This is not a single bottleneck story. It is the combined effect of geopolitics, tariff volatility, AI-led component allocation and renewed inflation in memory and processors. That combination makes 2026 feel less like a normal cyclical squeeze and more like a structural reset. The issue is not just shortage. It is interaction: each pressure point amplifies the others.

ENERGY SHOCK, ELECTRONICS IMPACT

The Strait of Hormuz may look like a distant geopolitical story, but for electronics it is a cost story hiding in plain sight. Roughly 20% of the world's oil and gas flows through that corridor. As disruption intensified in early March, Brent crude moved well beyond the low-$80s, broke above $100 per barrel and later reached as high as $119 intraday. Natural gas prices also jumped. For electronics vendors, that does not simply mean more expensive shipping - it points to a wider cost cascade across materials, logistics, warehousing and retail distribution.

TARIFFS: VISIBLE COST, INVISIBLE DISRUPTION

Tariffs have moved back to the centre of global sourcing decisions, with duty levels and sourcing advantages shifting faster than supply chains can adapt. Although US emergency-based tariffs were struck down by the U.S. Supreme Court in February 2026, Washington is actively rebuilding a broader tariff regime through other legal channels, which means more changes are likely in 2026.

Outman’s research in IT components highlights that the problem is not only the duty itself. The deeper problem is uncertainty around where to manufacture, where to import from, and how long today's cost assumptions will remain valid. As Maersk's product development manager William Petty has noted, tariffs increase costs and directly affect supply chains, pricing, profitability and ultimately the viability of a product in a particular market.

AI IS PULLING THE SUPPLY CHAIN UPHILL

The most important structural shift in 2026 is not political. It is architectural. AI infrastructure is now strong enough to reshape the semiconductor market around itself. AI servers require dramatically more memory per system than mainstream consumer devices, especially high-bandwidth memory and high-capacity DDR5 configurations. Some market forecasts suggest AI infrastructure could account for close to 70% of global memory-chip consumption in value terms in 2026. Whether the exact share lands slightly below that level or not, the direction is unmistakable: AI is taking priority, and the rest of the market is adjusting around it.

PROCESSORS, DRAM AND NAND: THE NUMBERS ARE GETTING HARDER TO IGNORE

What started as an AI boom inside data centres is now visible across mainstream hardware categories. Some forecasts point to DRAM and NAND price increases of around 80%-90% in Q1 2026 QoQ. Outman expects average PC prices to rise by around 15% in 2026, with more pessimistic scenarios moving closer to 20% for major brands. The jump from 64GB to 128GB of RAM, once a choice based on real user requirements, is now increasingly dictated by the scarce availability of lower RAMs. Users are obliged to opt for higher RAM options. Memory is no longer behaving like a routine bill-of-materials line; it is becoming a strategic constraint.

HOW THE INDUSTRY IS MOVING IN REAL TIME

Samsung reportedly raised memory-chip prices by as much as 60% compared to September as shortages worsened, while Micron has signalled that the shortage could persist beyond 2026. Memory-chip manufacturer Phison’s CEO, Pua Khein-Seng has gone even further, warning that NAND shortages in 2026 could be severe enough to shut down some consumer electronics companies. There are also signs that pressure is spreading into procurement strategies. Reports have indicated that HP, Dell, Acer and Asus have explored the use of Chinese memory suppliers such as CXMT as they look for alternatives to leading brands such as Samsung, SK Hynix, and Micron.

Figure 1. Selected cost signals visible in early 2026. Source: Reuters, TrendForce.

A MARKET WITH LESS ROOM FOR ERROR

Put simply, 2026 is becoming a year in which procurement mistakes will be punished more quickly. A brand that buys too late may miss allocation. A brand that prices too aggressively may destroy margin. A brand that assumes energy, customs and memory costs will normalise quickly may find its planning window has disappeared. This is no longer just a squeeze. It is a hierarchy: the largest AI buyers are locking in capacity, and everyone else is adapting to what remains.

IMPLICATIONS FOR THE IT SUPPLY CHAIN

Whether you are an OEM, a distributor or a buyer you will need to:

1. Build more flexibility into product and purchasing plans, especially where memory specifications add cost without materially improving end-user value.

2. Stress-test sourcing exposure by component, geography and tariff pathway rather than relying on historical procurement logic.

3. Move critical purchasing decisions earlier and treat selective inventory buffers as protection against allocation risk and price spikes.

The perfect storm is here and will be a stress test for players throughout the IT supply chain. Proactively reacting to commercial disruption can make a difference between survival and failure.

Outman provides ad-hoc strategic market analysis reports to answer specific questions of ICT market intelligence teams regarding market sizing, key trends and forecasts. Visit outmanconsulting.com or contact Outman at info@outman-consulting.com to access “The Personal Electronics Perfect Storm” full report.